November 26, 2023

Guyana has taken its long-standing territorial dispute with Venezuela to the International Court of Justice, seeking an order to halt Venezuela's planned referendum on the oil-rich Essequibo region.

November 26, 2023

Iran anticipates an increase in oil production to 3.6MM b/d by Mar. 2024, up from the current 3.3MM b/d.

November 26, 2023

The continent is anticipated to experience a gradual decline in oil production in 2024, according to insights from the African Energy Chamber.

November 26, 2023

Amid the accelerating energy transition, oil refiners are facing a challenging landscape, prompting forecasters to highlight the impending drop in fuel demand and a shift toward petrochemicals as a primary revenue source.

November 26, 2023

The International Energy Agency (IEA) has sounded a clarion call to the global oil and gas industry, underscoring the precarious nature of current investment levels in upstream projects.

November 26, 2023

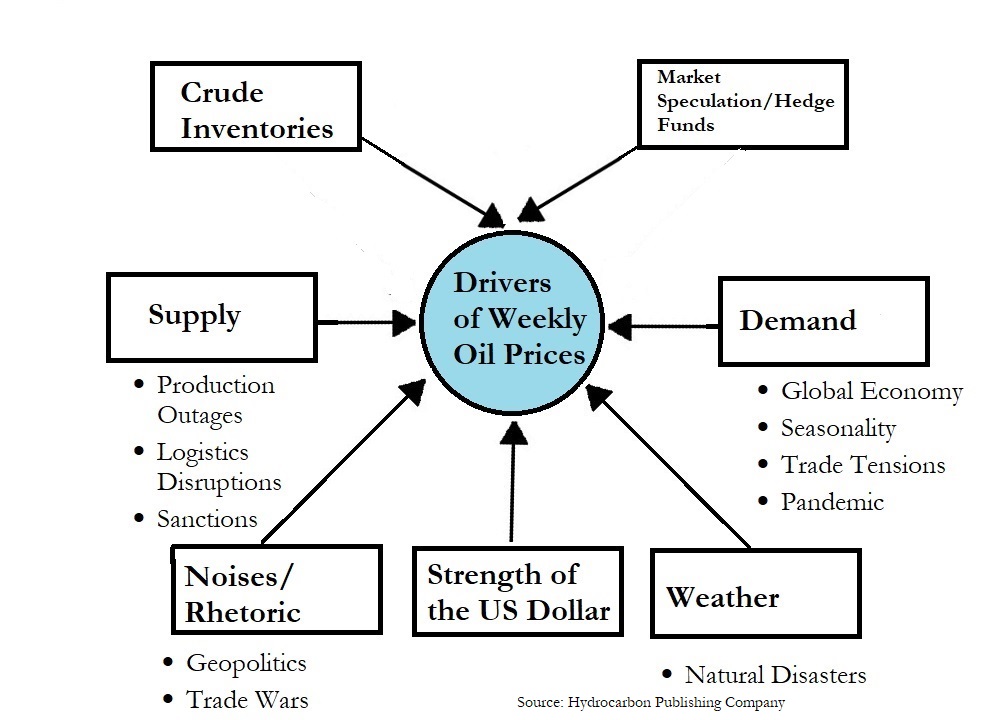

Prices for NYMEX WTI, ICE Brent, and DME Oman strengthened early in the week ending Nov. 24 amid expectations that OPEC+ would further cut production at its next meeting.

November 26, 2023

They are set to propose a landmark initiative at an upcoming OECD meeting, urging the world's wealthiest nations to cease subsidies for foreign oil, gas operations, and coal mining as reported by Financial Times.

November 20, 2023

A recent report by the Energy Transitions Commission highlights the indispensable role of carbon capture, utilization, and storage (CCUS) in certain industries' decarbonization efforts.

November 20, 2023

The International Energy Agency (IEA) has adjusted its predictions for global crude runs, anticipating an increase of 1.9MM b/d in 2023 and an additional 1MM b/d in 2024

November 19, 2023